Insights & Events

The latest thinking at your fingertips. Discover thought leadership, blogs, webinars, news, and more. Find it all here.

Insights & Events

The latest thinking at your fingertips. Discover thought leadership, blogs, webinars, news, and more. Find it all here.

More insights, right this way.

Press Releases

DFIN Introduces AI-Powered iXBRL Tagging for SEC Filings, Delivering Breakthrough Speed, Accuracy, and Control for Regulatory Compliance

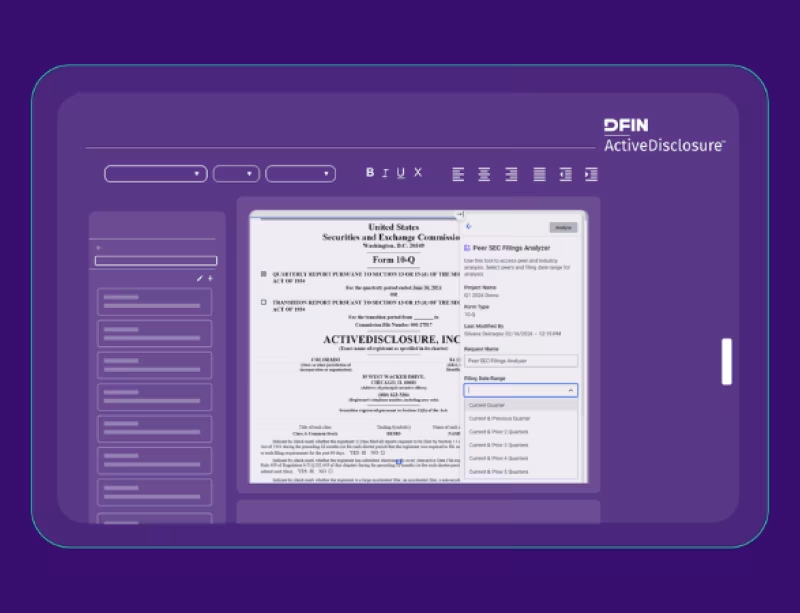

Blogs

From Compliance to Competitive Advantage: Why Peer Intelligence Is Redefining Financial Reporting

Press Releases