Whether you're a startup in search of capital to expand, a biotech in need of cash to advance their drugs through clinical development, or a portfolio company with investors looking to exit, you have choices. To determine what's best for your business and figure out how to choose an exit strategy, read on.

Business Exit Strategy Types

There are three common exit strategies available for private companies: an initial public offering or IPO, a direct listing, and a reverse merger with SPAC, commonly known as de-SPAC.

Initial Public Offering

The S-1 IPO is a traditional exit strategy for companies. In an IPO, companies sell a portion of their shares to the public. To sell your shares publicly, you'll need to register with the SEC — or Securities and Exchange Commission — and meet certain requirements related to publicly traded companies.

While you most often hear of "unicorn" companies with $1 billion valuations going public, or PE-backed portfolio companies, smaller companies can go public too. An IPO can take anywhere from 6-9 months, if not longer. There are financial disclosures, compliance and reporting requirements, and marketing pitches. Typically, executives make promotional pitches to potential investors in advance of the IPO, to ensure that there is a built-in audience ready to buy shares. Companies must also be prepared for the responsibilities they'll have toward their shareholders once the business is publicly held; they should also prepare for the rigors of the valuation process, which tends to be heavily influenced by market trends.

Before a company's stock is offered to the public, there is a valuation process that sets a value for the business, and thus for the new shares written in the IPO process. Underwriters will assess a range of factors, including demand for the company's shares (which can increase value), the potential future growth of the company, a compelling or unique story that can capture media attention, and the performance of its competitors. A company with strong growth potential, a charismatic founder or origin story, public clamor for shares, and peers who have preceded it with a successful IPO is more likely to receive a high valuation, while companies with fewer favorable trade winds will see a lesser valuation in advance of the IPO.

Direct Listing

A lesser-known aspect of an IPO is the cost associated with it. Every share costs the company a commission fee, which is paid to the underwriter. The commission generally varies from 3-7% of every share. After a successful IPO, a company may pay millions to the underwriters who enabled the process. Companies that don't have — or don't want to spend — the money may prefer a direct listing.

A direct listing is typically faster and cheaper than an IPO, and there's no need to take the sales pitch on the road. In a direct listing, the company is able to sell shares directly, without needing the assistance of intermediaries.

While the process is quick, it's not immediate; direct listings generally take anywhere from 6 to 9 months. There are risks associated with direct listing, too: Namely, there's no guarantee that anyone will be interested in buying shares and initial share prices will be subject to the volatility of the market.

De-SPAC

The de-SPAC option may be attractive for companies that lack the unique buzz associated with big-name IPOs. The businesses themselves are no less worthy of investment than the Silicon Valley unicorns, but they may operate in a market sector that's fallen out of favor among the investment crowds. Like the direct listing, the de-SPAC option is faster and cheaper than an IPO. A de-SPAC, or SPAC reverse merger, requires the filing of a Form S-4 and takes three to four months to accomplish.

In this strategy, a company is taken public through a merger with a SPAC that is already publicly held. There is generally a road show where you make your case to potential partners. The two companies first come to agreement on the terms of the merger, which includes a valuation for the company you wish to sell. While the costs of this approach can rival those of an IPO, it is the fastest exit strategy and should be considered when time is of the essence.

How DFIN Can Help With Your Exit Strategy

Whether you're interested in an IPO, direct listing or de-SPAC, DFIN can help you execute your exit strategy.

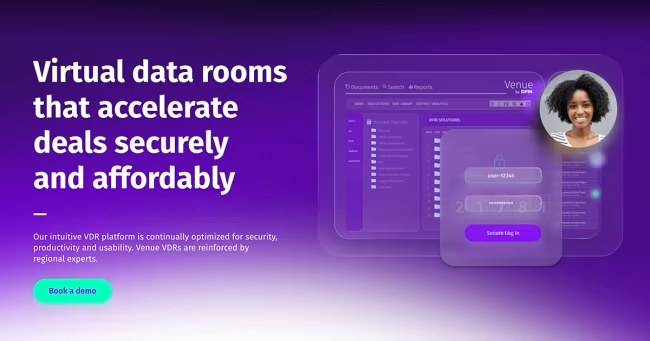

Clients have access to our virtual deal room, Venue, before the transaction and throughout the entire process. Within the virtual deal room, you can set permissions as to who can view files and folders; use watermarks and expiration dates to build in security; customize agreements with notes to users; use Venue's audio-redact tool when there's confidential information.

Once the transaction is complete, clients are able to use ActiveDisclosure to meet any SEC filing requirements and complete their financial reporting. ActiveDisclosure includes collaboration tools and workflows, versioning and track changes for consistency, and the ability to import financials directly from Excel for accuracy. It is cloud-based and secure, and there's an expert ready to help 24/7 should you need assistance.

The experts at DFIN have helped companies of all sizes go public, and we're here to help your business with its next steps. Get the assistance you need from a team that offers end-to-end solutions for your business journey.